Since 2013, only annuity and linear mortgages are eligible for mortgage interest tax deduction in the Netherlands. To qualify, the loan must be fully repaid within 30 years.

Other types, like interest-only mortgages, often offer lower monthly payments but do not qualify for tax benefits and come with higher long-term financial risk.

Choosing the right mortgage structure depends on your income, financial goals, and how much certainty you want.

💡Get independent advice to find the mortgage that fits both your current situation and future plans.

With an annuity mortgage, you pay a fixed monthly amount that includes both interest and repayment. Initially, most of the payment goes toward interest. Over time, the interest portion decreases while the repayment increases.

Key Features

Fixed monthly payments

You pay the same gross amount every month (interest + repayment), providing clarity and stability in your budget.

Shifting payment structure

Initially, your payments consist mostly of interest. Over time, repayment takes up a larger share.

Fully repaid after 30 years

At the end of the term, the mortgage is fully repaid. Interest may be tax-deductible for up to 30 years (if applicable).

Ideal for buyers looking for stable monthly payments and long-term financial security.

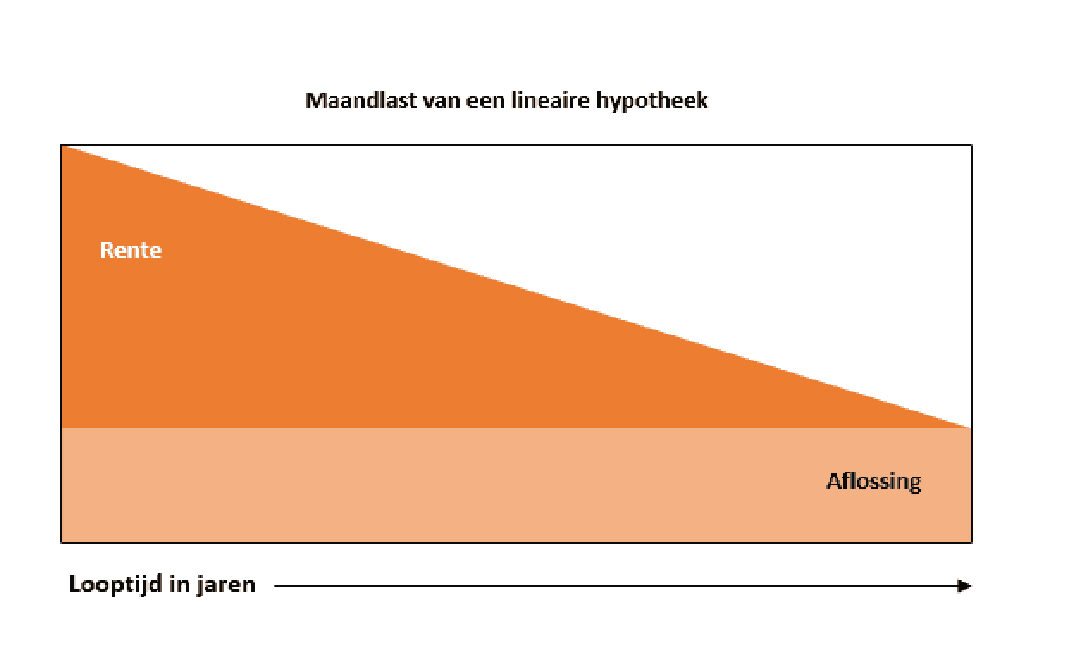

With a linear mortgage, you pay a fixed amount of the loan principal every month. As your outstanding debt decreases faster, your interest costs – and therefore your monthly payments – also go down over time.

Key Features

Fixed monthly principal repayment

Each month, you repay the same amount of the mortgage.

Decreasing monthly payments

As the loan balance drops, you pay less interest, which reduces your total monthly costs.

Ideal for buyers who want to repay their mortgage faster and reduce overall interest costs.

With an interest-only mortgage, you pay only interest during the loan term. The full loan amount remains outstanding and must be repaid in full at the end of the mortgage term.

Key Features

Interest-only payments

No repayments are made during the term – you only pay interest.

Lower monthly costs

Monthly payments are relatively low because you’re not repaying the loan yet.

Full repayment at the end

The entire loan must be repaid in one lump sum at the end. New interest-only mortgages are not eligible for tax deductions.

Ideal for buyers seeking low monthly payments and who have a clear repayment strategy for the end of the term.

The right mortgage starts with the right advice.

At Home Financials, we go beyond the numbers – we consider your personal goals, lifestyle, and future plans.

Together, we’ll find the mortgage structure that truly fits you: clear, personal, and 100% independent.

Heb je een vraag?

Bel: +31 621227373

Mail naar: info@homefinancials.nl

Erkend Financieel Adviseur (SEH)

Onze adviseurs zijn SEH-gecertificeerd en volgen jaarlijks bijscholing.

Zo ben je verzekerd van deskundig, betrouwbaar en actueel advies.

Heb je een vraag?

Bel: +31 621227373

Mail naar: info@homefinancials.nl